| Follow us on:

|

The Least Loved Commodity

Oil is old fashioned. There is virtually nothing about the stuff that excites a modern day “thought leader” or an aspiring business journalist. It’s filthy, it’s ecologically dangerous, it’s been produced on an industrial scale for well over a century, it isn’t renewable, and, at least for the ignorant, it seemingly doesn’t require any skill to produce.

Perhaps even more importantly, oil is almost always found either in hardscrabble rural areas or in the middle of the ocean. No one in the fashionable places of the world, places like Mayfair, Georgetown, Tribeca, or any of the other handful of places where the genuinely rich and powerful, and their journalist and politician hangers-on, gather and socialise is going to go and simply “hang out” at an oil derrick the way they might go visit the local Google, Apple, or Facebook office. And nor will their friends be “oil men” the way that they might very well be lawyers, consultants, programmers, bankers, or entrepreneurs of various stripes.

And so because oil is old fashioned, and because it is produced in far-off, scary, and distasteful places, places where the people are viewed as poorly dressed, uncultured rubes, many seem to think that it doesn’t matter. Green energy is fashionable, after all, not those dirty hydrocarbons. The future belongs to the “smart grid” and the wind farm, not the pipeline and the pumping station.

And if you are somehow able to get the mainstream media to admit that oil genuinely matters (a very big if) they will immediately counter that it “ought not to count” because oil is not something that is made but something that is, to use the most frequent cliché “just pumped out of the ground.”

In the latest entry of his never ending series on Russia’s impending economic collapse, Owen Matthews, the Russia correspondent for Newsweek before that wretched magazine finally met its long overdue end, even went so far as to label oil earnings “free money” that (as if by magic!) simply “comes bubbling out of the ground.”

![Oil wells in Siberia. [Getty Images]](http://thebricspost.com/wp-content/uploads/2013/01/Oil-Russia-300x211.jpg)

Oil wells in Siberia. [Getty Images]

It’s true that Matthews has his own unique peccadilloes about Russia, but in his palpable disdain for oil and everything associated with it, as well as in his airy assumptions that, because oil is primitive it should be cheap, he is very much in line with a press corps that values the new, the bold, the original, and the daring at the expense of the old and boring.

Indeed, ever since the price of oil started to truly spike back in 2005, I can remember reading, with increasingly humorous regularity, pronouncements about the coming collapse in oil prices in publications like The Economist and The Wall Street Journal. These articles were very long on the details about how inconvenient expensive oil was for developed industrial countries, but, apart from a general sense of nostalgia about the cheap-oil fueled 90’s, were very short on any arguments as to why oil should actually be cheap. The argument was, without exaggerating too greatly, “oil should be cheap because oil should be cheap.”

Oil after the global financial crisis

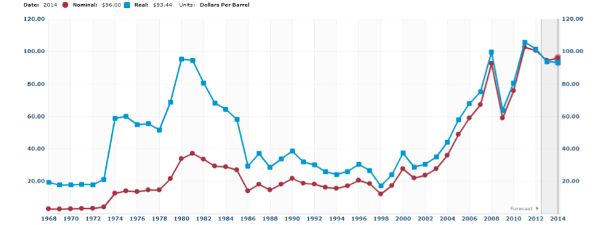

During the peak of the pre-crisis bubble in 2008, right around the time of the Beijing Olympics, oil prices briefly surpassed the all-time inflation-adjusted high that they had reached the massive price spike of the early 1980’s. Consider the following chart, where the blue line is the real price of oil (in 2012 dollars) and the red price is the nominal. The mid to late 1980’s and the entirety of the 1990’s saw low oil prices, so many people simply so used to $20 a barrel oil that they viewed it as an immutable part of the world.

Once the bubble burst, of course, oil prices rapidly plummeted and, in 2009, averaged out as almost 50 per cent cheaper than they were in 2008. At the time, many heralded a new era of cheap energy, blaming the pre-crisis run-up in prices on everybody’s favorite boogeyman: speculators. Things were “back to normal” and Russia and all of the other large energy producers, who had gotten a little too big for their britches, were going to have to go on a diet.

But after that temporary collapse, something very curious happened: the price of oil rapidly rebounded in 2010 and continued to climb relentlessly throughout 2011. It might seem hard to imagine that, in a year that saw the eruption of a full-blown debt crisis in the world’s largest unified market, and decidedly sub-par growth in the single most economically significant country, natural resources would become much more expensive. But 2011 was the most expensive that oil has ever been. And 2012 prices were only marginally cheaper, with the average for the year actually higher than the average price during the supposedly frenzied and out of control bubble days of 2008.

In contrast to much of the 1970’s, when the shortage of oil was an explicitly political construct created by OPEC to punish the West, 2011 saw a much broader array of producers producing at or near their all-time peaks. While it is true that the Saudis, as ever, were lurking in the background with an unknown and likely unknowable amount of surplus capacity, the world oil market these days is not nearly as OPEC-heavy as it was forty years ago.

How the BRICS fit in

Some observers such as Avazier Tucker in the recent version of Foreign Affairs, have argued that “tight oil,” oil produced from shale and other hitherto inaccessible geological formations, will lead to a future of cheap, plentiful energy. In this understanding the United States is mere years away from the previously unimaginable situation of “energy independence,” and this will represent a crushing blow to Russia and other large exporters.

However other far more reputable organizations, such as the International Energy Agency and the United States’ Energy Information Administration forecast a slow, steady increase in the real price of oil over the next 20 years, and also forecasts rapid supply growth from non-traditional producers such as Brazil (the potential of Brazil’s pre-salt oil formations are one of country’s main selling points, but these formations are only commercially feasible if oil prices stay high).

I should be clear in saying that I lean towards the EIA view, but there are few questions more important to the future of the world economy than finding out who is right. And not just for a large oil producer such as Russia or a potential large producer such as Brazil, for large importers and consumers such as India and China as well.

As should be clear from looking back over the past decade, industrialised countries do not tend to do perform very well economically when energy is expensive. There is a reason that the energy shock of the 1970’s, when supplies were cut off and prices soared to dizzying heights, still conjures something approaching pure terror in Western policymakers. Developed industrial societies consume absolutely enormous quantities of energy, particularly when compared to the still relatively underdeveloped BRICS, and the more expensive this is, the more their consumers suffer.

When it comes to oil, the BRICS still have a lot of low-hanging fruit: there are, quite simply, many more instances where replacing human with machine power yields a meaningful economic return in China or India than in France or Germany. Thus while high oil prices certainly aren’t enjoyable from the BRICS perspective they are much less problematic because these countries do not have transportation infrastructures constructed largely on the assumption of $20 a barrel oil, nor do they, yet, have passenger car ownership rates anywhere near Western norms.

I know that it seems counterfactual, or perhaps even bizarre, that expensive natural resources would aid traditionally poor countries like China, India, or South Africa, but the BRICS gradual convergence towards Western levels of income actually accelerated during the 2000’s and the long run up in commodity prices.

Oil as a Foreign Policy Factor

While the BRICS have proven that they can thrive even in an environment of high oil prices, the underlying scarcity that such prices suggest is nonetheless problematic both for importers and exporters. In an environment of sustained oil scarcity, importers such as India and China will be forced to take more active international roles to protect shipping lanes and keep the oil flowing.

It’s highly unlikely that either of these countries will replicate America’s hyper-interventionist approach, they neither have the capability nor the desire to have such an outsized footprint in the Middle East, but it is perfectly reasonable to expect a more visible presence on the world’s oceans for the Chinese and Indian navies (both which are being rapidly upgraded with new kit, including aircraft carriers).

Brazil and Russia, both of which are going to be spending massive sums of money constructing new offshore platforms over the coming decades, will obviously be interested in protecting their new assets. It’s therefore fair to assume that both countries are also going to invest heavily in their naval capabilities, though this will be less of an expeditionary capacity and more focused on protecting and defending territorial waters.

![A Brazilian owned oil rig. [AP]](http://thebricspost.com/wp-content/uploads/2013/01/Oil-field1-300x200.jpg)

A Brazilian owned oil rig. [AP]

Expensive oil, then, will drive the BRICS to ever more visible and important international roles, as sustained tightness in oil supply will make any disruptions that much more disruptive and expensive.

Towards a brave new world of expensive energy

I don’t think that the future holds any great ruptures or titanic surprises. I think that “peak oilers,” the nickname for those who think that a catastrophic decline in oil supply is only a few years away, have significantly underestimated human ingenuity and the profit motive’s ability to drive companies to new heights of performance.

At the same time, I think that the supply optimists like Tucker severely underestimate the expense and the sheer difficulty of procuring oil from non-traditional sources. Wells drilled in the much hyped Bakken deposit in North Dakota, for example, have incredibly steep decline rates, and maintaining production requires ever-greater numbers of rigs. That sort of production is possible, but can only be sustained if oil prices remain very, very expensive compared to their historical average.

I think, basically, that we’ve reached a rough equilibrium in oil prices: if the price goes below $90, substantial supply comes offline because it’s no longer economical, and the price then gradually rises. By the same token, if prices go much higher than $110 then demand shrinks and the price gradually falls back down.

So my best guess is that, over the next decade, we’re going to see a rough continuation of the trends from the last one: the BRICS will slowly, but surely, continue to gradually converge with the West and commodity prices will be persistently stuck at levels that, to many Westerners, feel “artificially” high. But that is just a guess. What isn’t a guess is that plain, boring old oil will continue to have outsized importance in the way the world economy operates.

Mark Adomanis has contributed to a wide range of journalistic outlets including True/Slant, Salon.com, The National Interest, Foreign Affairs, and Forbes.Com, where he is a regular contributor. Adomanis has focused particularly on Russian health and demographics, though he also closely follows emerging Russian political and economic trends. He feels that Russia often gets short-shrift compared to the other BRICS, and looks forward to providing comprehensive and fair-minded analysis. He received his undergraduate degree in Government from Harvard University and his M.Phil in Russian and East European Studies from the University of Oxford in 2009.