| Follow us on:

|

![President Jacob Zuma said he had removed Nene as Minister of Finance to "another strategic position" [GCIS]](http://thebricspost.com/wp-content/uploads/2013/03/8588266845_69bb862792_o-e1364231401663.jpg)

President Jacob Zuma said he had removed Nene as Minister of Finance to “another strategic position” [GCIS]

“I have decided to remove Mr Nhlanhla Nene as Minister of Finance, ahead of his deployment to another strategic position,” Zuma said in a release sent out late on Wednesday evening.

“The new deployment of Mr Nene will be announced in due course,” Zuma added.

As there were few market participants active at the time, the rand went to a record R15.39 against the US dollar, but in early trade on Thursday it recovered to R14.86.

The rand had traded below R14 to the dollar as recently as November 25 after being near the R11.40 level in February this year.

The new finance minister, David Van Rooyen, previously served as a Whip of the Standing Committee on Finance and as Whip of the Economic Transformation Cluster.

He is a former Executive Mayor of Merafong Municipality and a former North West provincial chairperson of the South African Local Government Association.

Concerns

The South African Chamber of Commerce and Industry (SACCI) said it was concerned about Zuma’s removal of Nene.

Nene had begun to find his feet after 18 months in the post and brought with him a number of years’ experience as Deputy Finance Minister.

“For SACCI and the business community at large, the consistency of our macro-economic policy environment is of paramount importance for trade and investment. Any major decisions which have a material impact on creating confidence must be weighed up carefully,” the business body said.

“As an important and key stakeholder, we are looking forward to the President sharing the motivation for this decision with the business community as a matter of priority,” it added.

Meanwhile, Nomura brokerage economist Peter Attard Montalto, who is based in London, said that R16 to the dollar was no longer an outrageous target.

“It is difficult to define where the upside target is, especially into December liquidity. However, 16 seems not an outrageous target. We will have to see where the rand settles, but in light of today’s event, our forecast will have to shift to see less chance of recovery from weak levels in the coming quarters as this credit story takes hold,” he said.

Fiscal discipline in the balance

Barclays Africa economist Peter Worthington said the sudden removal of the high profile and respected Nene and his replacement with a relative unknown was likely to be seen as a worrying signal about the government’s commitment to fiscal discipline and generate further market volatility.

“The quick sell-off, in our view, is a sign that that the markets are initially interpreting the cabinet reshuffle as a blow to the institutional credibility of the National Treasury,” he said.

Nene pointed out in October at the time of the Medium Term Budget Policy Statement that if there was no fiscal consolidation, then interest payments on government debt would soon exceed transfers to the 16.4 million social assistance beneficiaries.

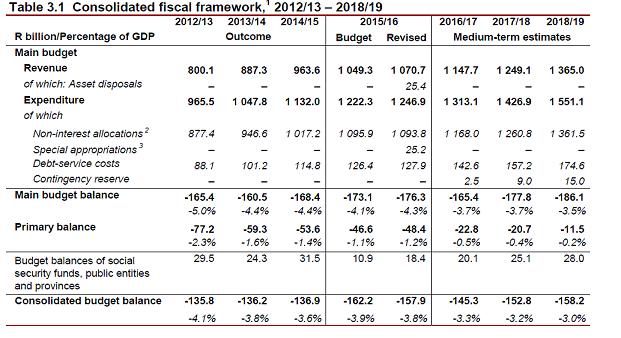

The debt service costs are projected to almost double from 88.1 billion rand in the 2012/13 fiscal year to 174.6 billion rand in 2018/19.

Source: South African Treasury

The government intends to issue foreign bonds at the rate of $1 billion per year over the next few years. It will primarily issue in the currencies in which it has liabilities, so no diversification in terms of foreign currency exposure is expected.

The government’s gross exposure to foreign currency loans is less than 10 per cent of total government debt.

Treasury officials told The BRICS Post that they would consider issuing in Chinese yuan once the Chinese capital market lengthened its maturity profile, as most issues there are now in the five to seven-year area, whereas Treasury would prefer to issue in the ten to twelve-year area.

By Helmo Preuss in Pretoria for The BRICS Post