| Follow us on:

|

The Medium Term Budget Policy Statement (MTBPS) on 25 October 2017 will be the first time that new Finance Minister Malusi Gigaba will be able to put numbers to his fiscal policy. Since taking over from Pravin Gordhan in April, Gigaba has emphasized that there will be fiscal policy continuity.

South Africa remains a lucrative buy, experts at a local conference said, despite the ratings downgrade. File photo: The Mall of Africa in Midrand, near Johannesburg, South Africa [Xinhua]

At the beginning of the MTBPS in 2016, the National Treasury set out the key concerns and constraints as follows:

“Difficult decisions will be made to ensure sustainable public finances. The MTBPS puts forward measured proposals to narrow the budget deficit and stabilise debt. Without taking these steps, we risk opening the door to rapid capital outflows and further economic disruption, setting back transformation, and leading to higher unemployment and social distress.

Citizens are registering their concerns. They want government to talk less and achieve more, act decisively against corruption and waste, contribute to growth and job creation, and speed up inclusive transformation and social justice. Much depends on joint action to restore confidence and mobilise private investment to avoid a low-growth trap.”

The problem is that since October 2016, South Africa entered a technical recession, no commission of inquiry has been set up to investigate allegations of state capture, the 9-point plan of action has not seen an public update since June 2016 on the progress of implementation, while business and consumer confidence was impacted by the March 2017 and October 2017 cabinet reshuffles.

The focus of economists and ratings agencies is on how Gigaba will present economic growth and the inflation outlook, which will feed through into revenue and expenditure assumptions and options for closing any revenue shortfall.

Crucial in this set-up is what to expect from the public sector wage bill and how this will influence the debt dynamics and rating agencies’ concerns about bailing out State-owned Enterprises (SOEs). One of the ways of encouraging growth has been to boost infrastructure spending, but there has been a gap between words and actions.

Slowing growth

In July, the South African Reserve Bank halved its forecast for 2017 growth to 0.5 per cent from a previous forecast of 1.0 per cent.

The September Beeld consensus forecast for growth this year is 0.6 per cent. In the first half of 2017, the economy grew by 1.1 per cent year-on-year (y/y) and August and September data point to an acceleration as exports grew by 15.2 per cent y/y in August to a record R103.4 billion, while new vehicle exports jumped by 11 per cent y/y to a record 36 359 units and new vehicle sales increased by 7 per cent y/y in September, the fourth consecutive month of y/y increases.

The bottom line, however, is that the National Treasury will be fiscally conservative and most likely use the economists’ consensus forecast of 0.6 per cent for growth this year and 1.2 per cent for next year.

Inflation has been moderating due to slowing food inflation this year with August consumer inflation at 4.8 per cent y/y. For MTBPS purposes however, the GDP deflator is more relevant as that is a key determinant of revenue growth, but the media very seldom report on this, so it is not top of mind amongst the public.

As the GDP deflator is impacted more by commodity prices and the exchange rate than the consumer inflation, there is likely to be a gradual acceleration to the 6 per cent level from 5.2 per cent y/y in the second quarter and 4.5 per cent y/y in the first quarter, when the rand was relatively strong.

Currently the consensus view (based on slow growth) is that there will be a R50 billion revenue shortfall this fiscal year, but the range is wide as it extends from R33 billion to R60 billion. This may be too pessimistic as growth is picking up, but as yet there has only been one month this fiscal year when revenue growth has exceeded expenditure growth. The 24 per cent y/y drop in the fiscal deficit in August hardly got any media coverage.

National Treasury will most probably choose the R50 billion revenue shortfall and then the political discourse is on how to close that gap. As in the February 2017 Budget, that gap will be closed by an increase in taxes (wealth and sin taxes), as well as the disposal of some state assets. The specifics of that are normally left for the February Budget, but this MTBPS may be an exception and a more detailed funding proposal could be spelt out.

Two global bonds

There was very little media coverage of the two global bonds worth US$2.5 billion issued on 20 September 2017. $1 billion was allocated to the 10-year bond and $1.5 billion to the 30-year bond.

Overall the bonds received bids of just over $5.3 billion – $2.1 billion in the 10-year and $3.2 billion in the 30-year tranche. The 10-year bond was priced at a coupon rate of 4.85 per cent (at par value) which represents a spread of 260.5 basis points above the 10-year US Treasuries. The 30-year bond was priced at a coupon rate of 5.65 per cent (at par value) which represents a spread of 283.7 basis points above the 30-year US Treasuries.

There was no comparison with previous global bond issues in the media, which would have shown that despite the April 2017 ratings downgrade there was hardly any impact on pricing. The 30-year bond, which theoretically is riskier than the 10-year bond due to its longer duration, in fact achieved better pricing than a year ago.

In September 2016, the 12-year bond was priced at a coupon rate of 4.3 per cent (at par value) which represented a spread of 273.8 basis points above the 10-year US Treasury benchmark bond. The 30-year bond was priced at a coupon rate of 5.0 per cent (at par value) which represented a spread of 271.9 basis points above the 30-year US Treasury benchmark bond. This R33.9 billion inflow will boost foreign reserves and reduce the call on the domestic bond market by an equivalent amount.

The favourable overseas perception of South Africa’s debt dynamics is reflected in the fact that foreigners have so far bought a net R68 billion worth of bonds in the first nine months of 2017.

The Treasury borrowed R158 billion in the first half of the fiscal year, while the full fiscal year borrowing was forecast at R188 billion. The second half of the fiscal year tends to be stronger from a revenue collection point of view as it includes the Christmas season sales in December and the individual tax-year end receipts in February. As mentioned previously, the consensus is for a R50 billion revenue shortfall, which would boost the borrowing to R238 billion.

State-owned enterprises (SOE) have faced a buyers’ strike as institutions such as Futuregrowth worry about state capture and corporate governance. In 2015/16, borrowing by the six largest state-owned enterprises – the Airports Company of South Africa (ACSA), Eskom, SANRAL, SAA, the Trans-Caledon Tunnel Authority (TCTA) and Transnet – reached R128 billion.

In the February 2017 Budget, the six companies projected aggregate borrowing of R102.6 billion in 2016/17, and R307.1 billion between 2017/18 and 2019/20.

Moody’s Investors Service and S&P Global Ratings will update their ratings on 24 November after the MTBPS, but will likely make some comments the evening of the MTBPS or shortly after.

Fitch is expected to update its rating in November, but has made no announcement on the scheduled date. Economists expect the ratings agencies’ to focus on SOE issues, where there can be more details in terms of announcements with credit implications especially regarding SAA and Eskom.

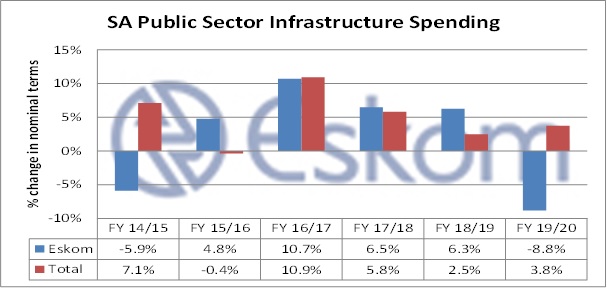

A key thrust of government’s growth plan since the 2008/9 Global Financial Crisis has been an emphasis on public sector infrastructure spending.

The problem is that this spending has been over budget and way behind schedule.

For instance Transnet’s Durban to Johannesburg Multi-Product Pipeline took nine years instead of three years to complete and the cost escalated from R12.7 billion to R30.4 billion. In addition, this spending is expected to slow in real terms as the Medupi and Kusile power stations bring units online.

Helmo Preuss in Grahamstown for The BRICS Post