| Follow us on:

|

Gordhan’s firing at the end of March weakened investor confidence and ultimately GDP growth [Xinhua]

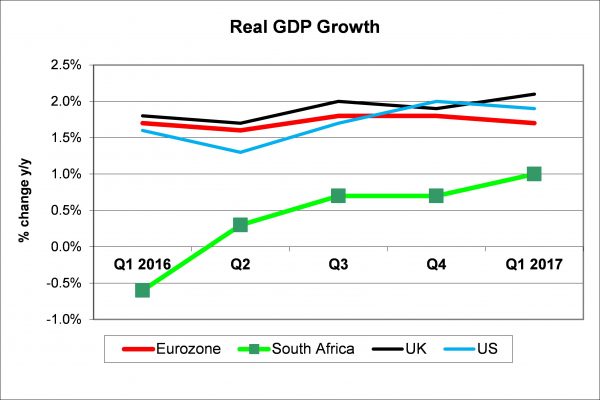

The optimists focused on the steady improvement in the year-on-year (y/y) growth rate that has increased from a dismal -0.6 per cent y/y in the first quarter 2016 to 1.0 per cent y/y in the first quarter 2016.

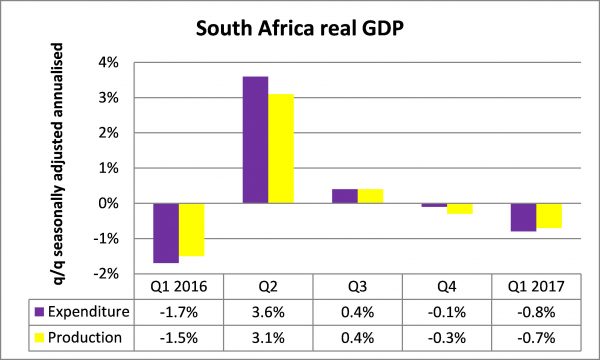

The pessimists focused on the 0.7 per cent quarter-on-quarter seasonally adjusted annualised (saa) contraction in the first quarter 2017 after a 0.3 per cent drop in the fourth quarter.

As the generally accepted definition of a recession is two consecutive quarters of contraction in the quarterly change, South Africa officially entered a recession for the first time since 2009.

Unlike 2009, the downturn this time is largely self-inflicted, as politics have impacted on business and consumer confidence. In 2009, it was a freeze-up in the global financial system that caused a global downturn, which South Africa as a small open economy could not escape.

Rand sell-off

The financial market participants took the pessimists view and sold off the rand after the GDP data.

If we compare the 6 cents per US dollar move from R12.79/$1 at the time the data was released at 11h30 (09h30 GMT) to R12.85/$1 in the first 15 minutes after the release, then this was a tiny move compared with the financial market responses to the political decisions to fire Finance Minister Nhlanhla Nene in December 2015 and Finance Minister Pravin Gordhan in March 2017.

In terms of detail, the production measure of GDP showed that the weakness in the first quarter was broad-based with only the agriculture and mining sectors expanding out of the ten production sectors.

Without growth in the primary sector, GDP would have contracted by 2.0 per cent. The biggest contributors to the decline were the trade sector, which contracted by 5.9 per cent q/q saa, and manufacturing, which declined by 3.7 per cent.

If one puts on the rose-tinted spectacles, then the y/y growth rates show declines in only four sectors with electricity down 1.6 per cent, trade contracting by 1.0 per cent, manufacturing declining by 0.9 per cent and construction slipping by 0.4 per cent.

The most noteworthy feature of the first quarter 2017 data was the recovery in agricultural production.

Record harvests

This showed the first q/q increase since the fourth quarter 2014 and was up a massive 22.2 per cent q/q saa, while the y/y growth was an equally impressive 10.3 per cent.

The positive impact will only truly be felt from the second quarter onward as the record maize and soybean crops are harvested from May through to September.

Please bear in mind that Brazil has just exited a two-year recession in the first quarter due to record soybean production, while the US economy received a large boost in the third quarter 2016 due to its soybean exports.

The impact of the record maize and soybean harvest on their own will add 0.5 per cent to GDP growth this year, but it will also have a positive effect on their forward and backward linkages as they will be able to buy more seeds, fertilizers and farming equipment at the start of the planting season in August, while the bountiful harvest will benefit feedlot operators as well as providing employment for the transport sector as the maize has to be stored in silos and/or shipped to overseas customers.

These effects could add a further 0.5 per cent to GDP growth. Higher employment and greater farming income will improve the lives of retailers as well.

Families spend less

From the expenditure side, final consumption expenditure by government contracted by 1.0 per cent in the first quarter, while household consumption expenditure fell by 2.3 per cent as families spent less on discretionary items such as clothing (-12.7 per cent), recreation (-8.5 per cent) and restaurants and hotels (-8.6 per cent).

The good news was that gross fixed capital formation continued to grow for the second consecutive quarter after contracting for four successive quarters.

Businesses also became more optimistic as they added to their inventories in expectation of higher sales once the record maize crop is harvested.

Large increases in inventories were reported for wholesale trade and the transport, storage and communication industry, but these stock builds were partially offset by a drawdown of inventories in the manufacturing sector as production could not keep up with demand.

The latter is good news for manufacturing as production needs to be ramped up to rebuild inventories and to satisfy demand from neighbouring countries as their improved agricultural production will lead to increased demand for South African manufactured goods.

Already the Mozambican economy has recovered from 1.1 per cent y/y growth in the fourth quarter to a 3.9 per cent y/y increase in the first quarter.

By Helmo Preuss for The BRIC Post in Johannesburg, South Africa